All Categories

Featured

Table of Contents

The drawbacks of boundless banking are usually forgotten or otherwise discussed whatsoever (much of the info readily available concerning this principle is from insurance coverage representatives, which may be a little biased). Only the cash worth is growing at the dividend price. You additionally need to pay for the expense of insurance coverage, costs, and expenses.

Companies that supply non-direct acknowledgment loans might have a lower returns rate. Your money is locked into a complex insurance product, and abandonment costs commonly don't disappear till you have actually had the plan for 10 to 15 years. Every long-term life insurance coverage plan is various, however it's clear a person's overall return on every dollar invested on an insurance policy item might not be anywhere near to the reward price for the policy.

Infinite Banking Calculator

To offer an extremely basic and hypothetical instance, let's assume a person is able to gain 3%, on standard, for every buck they invest on an "limitless banking" insurance coverage item (after all expenses and fees). If we presume those dollars would certainly be subject to 50% in taxes total if not in the insurance policy product, the tax-adjusted price of return could be 4.5%.

We assume higher than typical returns overall life product and a very high tax price on bucks not put into the policy (which makes the insurance product look far better). The reality for many individuals might be even worse. This pales in contrast to the lasting return of the S&P 500 of over 10%.

Unlimited banking is a wonderful item for agents that offer insurance policy, but might not be optimum when contrasted to the more affordable choices (without sales individuals gaining fat compensations). Right here's a failure of some of the other supposed benefits of limitless financial and why they may not be all they're gone crazy to be.

Banking On Yourself

At the end of the day you are purchasing an insurance policy product. We like the security that insurance policy offers, which can be acquired a lot less expensively from a low-cost term life insurance plan. Overdue fundings from the plan might likewise decrease your death advantage, diminishing another level of defense in the plan.

The idea only functions when you not only pay the substantial premiums, yet utilize added cash money to purchase paid-up additions. The chance price of all of those dollars is remarkable extremely so when you can instead be buying a Roth Individual Retirement Account, HSA, or 401(k). Even when compared to a taxable financial investment account or even a cost savings account, infinite financial may not provide equivalent returns (contrasted to investing) and similar liquidity, gain access to, and low/no charge framework (compared to a high-yield savings account).

With the increase of TikTok as an information-sharing platform, monetary suggestions and methods have discovered an unique way of dispersing. One such strategy that has actually been making the rounds is the limitless banking concept, or IBC for short, gathering endorsements from celebs like rapper Waka Flocka Flame. While the approach is presently popular, its origins trace back to the 1980s when financial expert Nelson Nash introduced it to the globe.

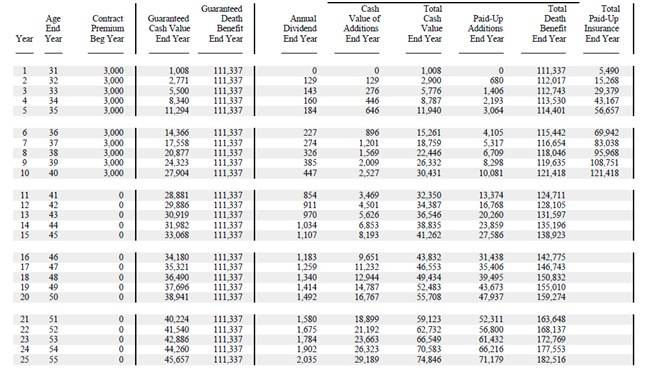

Within these policies, the money value expands based upon a price established by the insurance firm. Once a substantial cash value accumulates, policyholders can acquire a cash money value finance. These financings vary from conventional ones, with life insurance policy functioning as security, implying one might lose their coverage if loaning exceedingly without ample cash worth to support the insurance coverage costs.

Infinite Banking 101

And while the allure of these policies is obvious, there are natural limitations and threats, necessitating attentive cash money worth surveillance. The strategy's legitimacy isn't black and white. For high-net-worth people or service owners, specifically those utilizing methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and compound development can be appealing.

The allure of boundless financial does not negate its difficulties: Price: The foundational need, a long-term life insurance coverage plan, is more expensive than its term counterparts. Qualification: Not everybody gets approved for whole life insurance due to extensive underwriting procedures that can leave out those with specific health and wellness or way of living conditions. Complexity and threat: The intricate nature of IBC, combined with its risks, might discourage lots of, particularly when easier and much less risky choices are offered.

Assigning around 10% of your regular monthly revenue to the policy is simply not feasible for a lot of individuals. Part of what you read below is simply a reiteration of what has actually already been stated over.

So before you get on your own right into a scenario you're not planned for, recognize the following initially: Although the concept is commonly offered thus, you're not really taking a financing from on your own - ibc full form in banking. If that held true, you would not need to settle it. Rather, you're obtaining from the insurer and need to repay it with interest

Bank On Yourself Whole Life Insurance

Some social media messages recommend making use of cash money value from entire life insurance coverage to pay down credit report card debt. The concept is that when you repay the car loan with interest, the quantity will be sent back to your investments. That's not how it works. When you repay the lending, a section of that rate of interest goes to the insurance provider.

For the initial numerous years, you'll be repaying the commission. This makes it incredibly tough for your plan to accumulate value throughout this moment. Whole life insurance policy expenses 5 to 15 times much more than term insurance policy. Many people merely can not afford it. Unless you can afford to pay a few to a number of hundred dollars for the next years or even more, IBC won't work for you.

If you need life insurance, here are some useful tips to take into consideration: Take into consideration term life insurance policy. Make certain to go shopping around for the best rate.

Infinite financial is not a services or product supplied by a details establishment. Infinite banking is an approach in which you get a life insurance policy policy that collects interest-earning cash money worth and obtain car loans against it, "obtaining from on your own" as a source of funding. Ultimately pay back the lending and start the cycle all over once more.

Pay policy premiums, a part of which builds cash money value. Take a lending out versus the plan's cash value, tax-free. If you use this concept as planned, you're taking money out of your life insurance plan to purchase every little thing you 'd require for the rest of your life.

{kind=link}

Latest Posts

Non Direct Recognition Life Insurance Companies

Want To Build Tax-free Wealth And Become Your Own ...

Infinite Banking Vs Bank On Yourself